James Whittington is an independent Chartered Financial Planner. Since graduating from Cambridge University, he has built up over 15 years’ experience across the finance industry, covering investment banking; investment modelling and risk management within the Lloyd’s of London market; and personal financial planning.

We speak to hundreds of principal practice owners across the country every year and we hear the same things from practice owners time and time again. At only our last conference, people told me:

“I struggle to find good-quality staff and associates that will not cost me an arm and a leg”

“My costs are going up on all sides – energy, equipment, lab, staff, interest rates on the practice property mortgage and on my business loans”

In today’s world, practice principals are seeing their income reduce at the same time their personal outgoings are increasing. Energy costs, rising food prices, mortgage rate shocks, above-inflation school fee increases: it’s all enough to leave even the most successful practice owners feeling less flush.

However, one of the main problems with these very clear and present dangers is that they are just that – very present in nature. They demand immediate focus and attention.

Whilst you are fighting these fires, you may be missing the slow-burn problems – the ones that gradually build in the background… until it is too late.

Even taking into account the increased income from private work and a bigger lump sum on the sale of a business that private work brings, our analysis shows that dentists are facing a nasty cavity in their retirement funds.

A particularly key reason for this is the NHS pension. To put this in context: we have a number of retired NHS dentist clients who are comfortably living off NHS pensions in excess of £70,000pa that they accessed from age 60, plus their state pension and their other savings, investments and business interests.

Clients that we are taking on in their 40s and 50s, with retirement in mind in the next 5-10 years, have significantly lower NHS pension forecasts. These are quite often under £10,000pa and cannot be accessed without penalty until age 67 (and there are calls for this to be increased to 71).

This disrepancy is the result of years of tinkering with the pension itself. Depending on which version of the pension you’re on, you’ll have access to different benefits, and it’ll also affect your approach to the NHS Dental Contract, too. You can read more about the detail behind this here.

How can I ensure my NHS pension is enough for me in retirement?

In order to determine when you can retire, what you can afford to spend in retirement, whether you’ll have enough for care fees in the future and how secure your loved ones will be, you’ll need to factor in:

- The intricacies of the NHS pension

- Other sources of income

- Expected proceeds from a business sale

- Cash investments

- Plus other factors dependent on your personal situation

This is no easy task. To do this effectively for our clients, our starting point is always to create a Financial Life Plan (FLP).

We use sophisticated modelling software to project various different scenarios, show the impact of retiring earlier or later, gauge the consequences of a higher or lower business sale, and run lifeboat drills (to stress test the plan) against market crashes, ill health and early death situations.

More than ever before, our FLP projections show a need to build up funds outside of the NHS pension, in order to supplement retirement income and enable our clients to still have the retirement that they desire, whilst providing financial security for their loved ones.

And, as seen in our recent article, changes to the Lifetime Allowance and Annual Allowance have only muddied the waters further – but also provide planning opportunities you would do well not to miss out on.

Without this analysis, it is impossible to know whether you will be facing a shortfall – and therefore to understand what you need to do to tackle the problem. Ultimately, because finance is personal, there is no silver bullet.

This is why our Financial Life Plans are uniquely tailored to your individual circumstances, needs, goals and timeframes.

Let’s see how that might work in practice

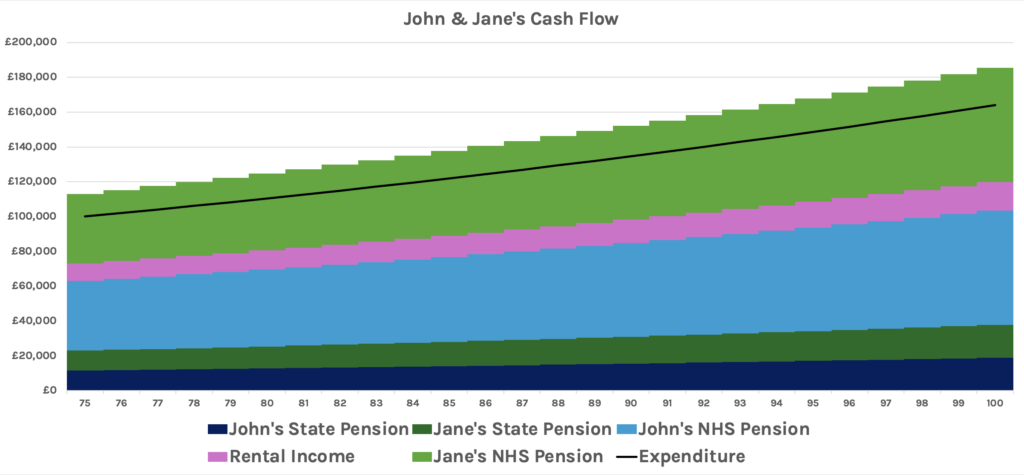

Here’s a typical example of the cashflow projection we might create for a couple who are already in retirement. John and Jane both have pensions that benefit from the more generous rates in the 1995 NHS contract scheme.

The black line represents expenditure and we can see that John and Jane are having no problems meeting their cashflow requirements.

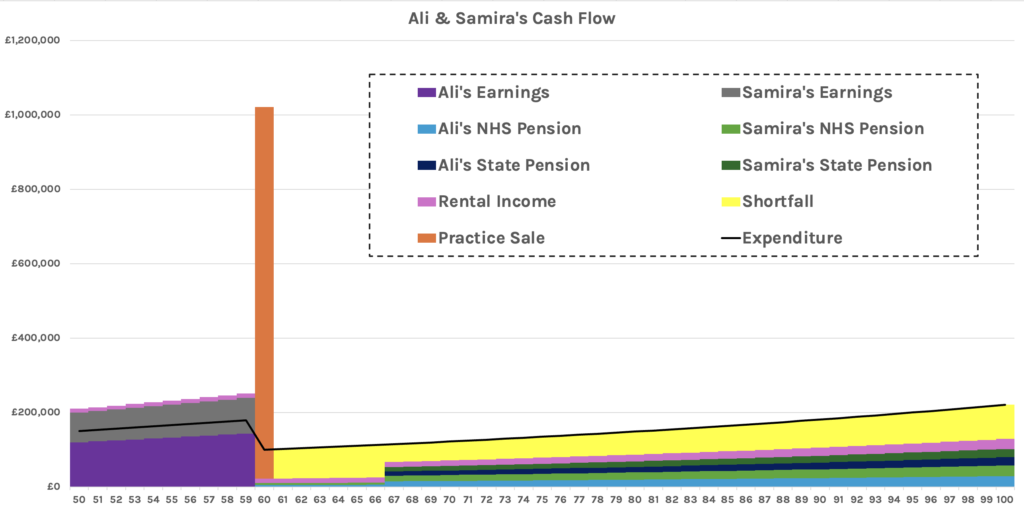

Ali and Samira, on the other hand, are in their 40s and both of them have pensions at the 2015 scheme rates. This chart is a little more complex. The couple would like to retire at 60, but our projections show that without action, this is currently unachievable.

Ali and Samira, on the other hand, are in their 40s and both of them have pensions at the 2015 scheme rates. This chart is a little more complex. The couple would like to retire at 60, but our projections show that without action, this is currently unachievable.

Note in particular the orange spike representing the practice sale, and the particularly fallow period before their NHS and state pensions kick in at age 67. Even when those pensions do kick in, expenditure (black line) is too great, and there is a shortfall (yellow).

Note in particular the orange spike representing the practice sale, and the particularly fallow period before their NHS and state pensions kick in at age 67. Even when those pensions do kick in, expenditure (black line) is too great, and there is a shortfall (yellow).

What Now?

As the old Chinese proverb says: “The best time to plant a tree was 20 years ago…the second best time is now”. The same is very much true when it comes to preparing for retirement.

Montgomery Charles are an independent financial planning company with nearly three decades of specialist experience advising dentist practice principals.

We are on hand to provide a complimentary, no-obligation consultation to help you on your journey. Book online via montgomerycharles.co.uk/bookachat, or contact us directly via 01225 777 999 / [email protected].