Montgomery Charles specialises in financial planning for principal dentists. With almost 30 years’ experience working in this sector, we’ve seen pretty much everything there is to see.

This resource aims to explain a bit more about two key areas that principals have to grapple with: the NHS Dental Contract, and the NHS Pension. Crucially, one affects the other: the way and the degree to which that you implement your contract can directly affect the pension you draw.

What’s covered in this resource

Jump to:

What is the NHS Dental Contract?

For a long time NHS contracts have been the backbone of the dentist industry. Dentists receive a Unit of Dental Activity (UDA) payment, the sum of which varies depending on the nature of the work undertaken (more detail on UDAs can be found here).

For a long time NHS contracts have been the backbone of the dentist industry. Dentists receive a Unit of Dental Activity (UDA) payment, the sum of which varies depending on the nature of the work undertaken (more detail on UDAs can be found here).

Historically, the UDAs that dentists received under the contract represented a great (and sometimes only) source of revenue. It offered good value in terms of the work required to fulfil each unit, and dentists were in very high demand due to a population with generally poor teeth.

Over time, through better education, knowledge (and a lot of hard work by the dental industry), people’s oral hygiene improved significantly. At the same time, a wealthier society found themselves with surplus income to spend. Coupled with the development of new treatments, this effectively created a new type of demand – the demand for more specialist treatments, both necessary and voluntary.

Throw in the increased cost of providing dental services, which has not been matched by a relative increase in the monetary value of UDAs, and many dentists today are turning away from the contract system.

The key problems dentists face with NHS contracts today

- In some cases, the UDAs allocated for types of treatment do not cover the cost of the work

- The upfront payments create an unnecessary creditor that may have to be repaid if a contract is not fulfilled

- The resultant penalties and limitations of not meeting a contract can make future business planning very difficult

- The shortage of associates within the industry means fulfilling contracts has become harder

- Private work (in particular, specialist work) is usually more profitable than NHS work

Why NHS contracts can still hold an attraction

During the Covid-19 pandemic, the NHS contract was a lifesaver for many practices and NHS associates. These groups continued to get paid, whilst the private equivalent received no income unless they had patients on plans paying monthly subscriptions.

And where you have guaranteed income, you tend to have higher practice valuations. Dentists are still mindful that NHS contracts have value in their stability and their superannuation pension, which exists in few places in commercial world.

The NHS pension, however, is a whole story in itself. Read on for more…

The NHS Pension – A Brief History

The complexity of the NHS pension is infamous: a culmination of legacy frameworks, with each new change looking to simplify things, but in fact further muddying the waters. Peeling back the layers, the main principle is as follows: providers get rewarded for providing NHS care, with a guaranteed inflation-linked income for life in retirement.

The level of income that dentists were set to receive in retirement was historically based on whether they were classed as an “officer” and/or a “practitioner”. Although this distinction between NHS workers still remains for previously accrued pensions, changes to the pension scheme means that is no longer the case.

Without getting stuck in the weeds, most dentists will be classed as practitioners, although some will have officer status and some will have both. In the 1995 and 2008 schemes, practitioners accrued NHS pension based on the value of the pensionable NHS contract work they had completed. This value benefits from ‘dynamisation’, which provides an uplift over time – essentially to offset the impacts of inflation, but typically at a more generous rate.

For officers, under the 1995 and 2008 schemes their NHS pension was based on their final salary. The 2015 scheme changed this, so that both practitioners and officers accrue their pensions based on the pensionable earnings in each year worked, revalued up to the date of retirement.

1995 and 2008: Huge changes

Over the last 30 years we have seen a major changes in the various NHS contract iterations: in how members build up their NHS pensions; how much they are likely to be able to draw in retirement; and when they can access their pensions.

The 1995 scheme is arguably the most generous, offering unreduced access from age 60 (55 for some), an automatic tax-free lump sum of three times the retiree’s annual income (without having to reduce the provided pension), and a 50% dependant’s pension.

The 2008 scheme had a slightly faster accrual rate, but offered no automatic lump sum (you had to reduce your pension income in exchange for tax-free cash), a smaller dependant’s pension of 37.5%, and individuals could not access their pension without penalty until the age of 65.

Both the 1995 & 2008 schemes stipulated final salary schemes for officers, and the ‘dynamisation’ method for practitioners.

A member could only have scheme membership under either 1995 or 2008 rules, not both. In fact, when the 2008 scheme was introduced members had the option to switch from 1995 – and a sizeable proportion did, despite it not being in their best interests.

2015: A further seismic shift

Everything changed in 2015. Accrual for both practitioners and officers was switched over to a Career Average Revalued Earnings (CARE) basis, which is typically less generous than a final salary basis. There is no automatic lump sum on offer. The dependant’s pension was reduced further to 33.75%. And most importantly for a lot of people, the age they can access their pension without penalty was linked to the State Pension Age (increasing to 67 and set to increase again to 68). This was a move echoed across the public sector pension landscape.

Unlike with the introduction of the 2008 scheme, members were not given a choice as to whether they were moved to the 2015 scheme for future accrual or not, although those who did get moved retained the benefits already accrued to date in their previous scheme.

To add another layer of complexity, existing 1995 & 2008 members who were close to retirement were provided transitional protection – which meant they were only moved over to the 2015 scheme at a date beyond the standard switch over, based on their age.

Then a ruling following two employment tribunals – concerning the pensions of judges and firefighters – shook up the landscape once again. The McCloud judgement further clouded the picture (pun intended) by saying that younger members had suffered age discrimination when the 2015 scheme was introduced as they had not benefitted from transitional protection.

At the time of writing, the consequence of this is that affected members will be offered the option to have their impacted membership years either classed under the 2015 scheme, or to be classed on a similar basis to whichever scheme they were a member of before the switch. It also introduced a final cut-off, meaning that from 1st April 2022 members could only accrue further membership under the 2015 scheme going forwards.

Balancing NHS and private practice: The challenges facing retiring dentists today

We’ve seen that the history of NHS dentists’ pensions is a complex one. But overall, there are a number of key issues that dentists who are working towards retirement must be mindful of:

We’ve seen that the history of NHS dentists’ pensions is a complex one. But overall, there are a number of key issues that dentists who are working towards retirement must be mindful of:

- Reducing the NHS work the practice secures will reduce the NHS pension you accrue going forwards

- Allocating the less-profitable NHS work to associates (so that the principals can carry out more-profitable private work) will reduce the NHS pension that principals accrue

- Ceasing all NHS work not only stops any future accrual, it will also sever the link for ongoing dynamisation (for practitioners) and to future salary increases (for officers with benefits previously built in the 1995 or 2008 scheme)

- Transitional protections aside, the NHS pension has progressively become less generous over time (i.e. from the 1995 to 2008 to 2015 schemes) and this trend is likely to continue over the coming decades

- It has become more and more complex to work out how much NHS pension you are actually entitled to (we occasionally see incorrect NHS reward statements) and therefore what you will have in retirement and when. It also makes it harder to understand the financial consequences of your decisions, such as whether you should reduce your pension to access it earlier and/or take a tax-free lump sum

- Survivorship issues are becoming more common, as surviving spouses and partners do not receive the income they once did

A lot of these issues – and their consequences – are going under the radar, especially against a backdrop of more immediate concerns such as increased cost pressures at both a practice and personal level.

In short – dentists are facing lower NHS pensions; can only access them later in life; and are not thinking about making up the shortfall due to prioritising more immediate concerns.

To put this into context, we have a number of retired NHS dentist clients who are comfortably living off NHS pensions in excess of £70,000pa that they accessed from age 60, plus their State Pension and their other savings, investments and business interests.

Clients that we are taking on in their 40s and 50s, with retirement in mind in the next 5-10 years, have significantly lower NHS pension forecasts. These are quite often under £10,000pa and cannot be accessed without penalty until age 67 (think tanks have recently called for this to be increased to age 71). Additionally their spouses and partners no longer have the financial security they once had, due to the double impact of lower members pensions and lower dependants’ pensions (33.75% instead of 50% of the member’s now lower pension).

How can I ensure my NHS pension is enough for me in retirement?

In order to determine when you can retire, what you can afford to spend in retirement, whether you’ll have enough for care fees in the future and how secure your loved ones will be, you’ll need to factor in:

- The intricacies of the NHS pension

- Other sources of income

- Expected proceeds from a business sale

- Cash investments

- Plus other factors dependent on your personal situation

This is no easy task. To do this effectively for our clients, our starting point is always to create a Financial Life Plan (FLP).

We use sophisticated modelling software to project various different scenarios, show the impact of retiring earlier or later, gauge the consequences of a higher or lower business sale, and run lifeboat drills (to stress test the plan) against market crashes, ill health and early death situations.

Even taking into account the increased income from private work and a bigger lump sum on the sale of a business that private work brings, our FLP breakdowns tend to show that dentists are facing a nasty cavity in their retirement funds. More than ever before, our recommendations focus on building up funds outside of the NHS pension to combat this increasing shortfall, in order to supplement retirement income and enable our clients to still have the retirement that they desire, whilst providing financial security for their loved ones.

Without this analysis, it is impossible to know whether you will be facing a shortfall – and therefore to understand what you need to do to tackle the problem. Ultimately, because finance is personal, there is no silver bullet.

This is why our Financial Life Plans are uniquely tailored to your individual circumstances, needs, goals and timeframes.

Case Study: Let’s see how that might work in practice

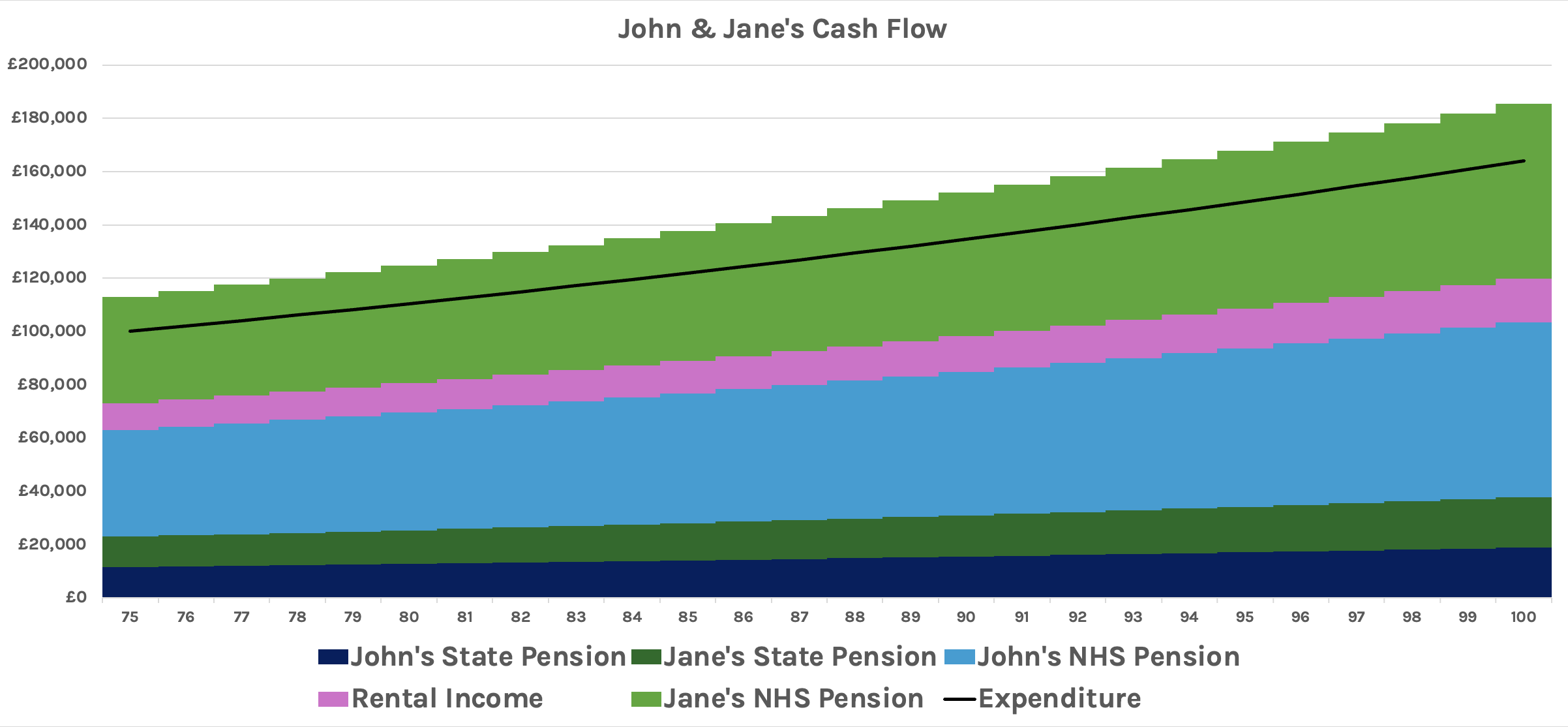

Here’s a typical example of the cashflow projection we might create for a couple who are already in retirement. John and Jane both have pensions that benefit from the more generous rates in the 1995 NHS contract scheme.

The black line represents expenditure and we can see that John and Jane are having no problems meeting their cashflow requirements.

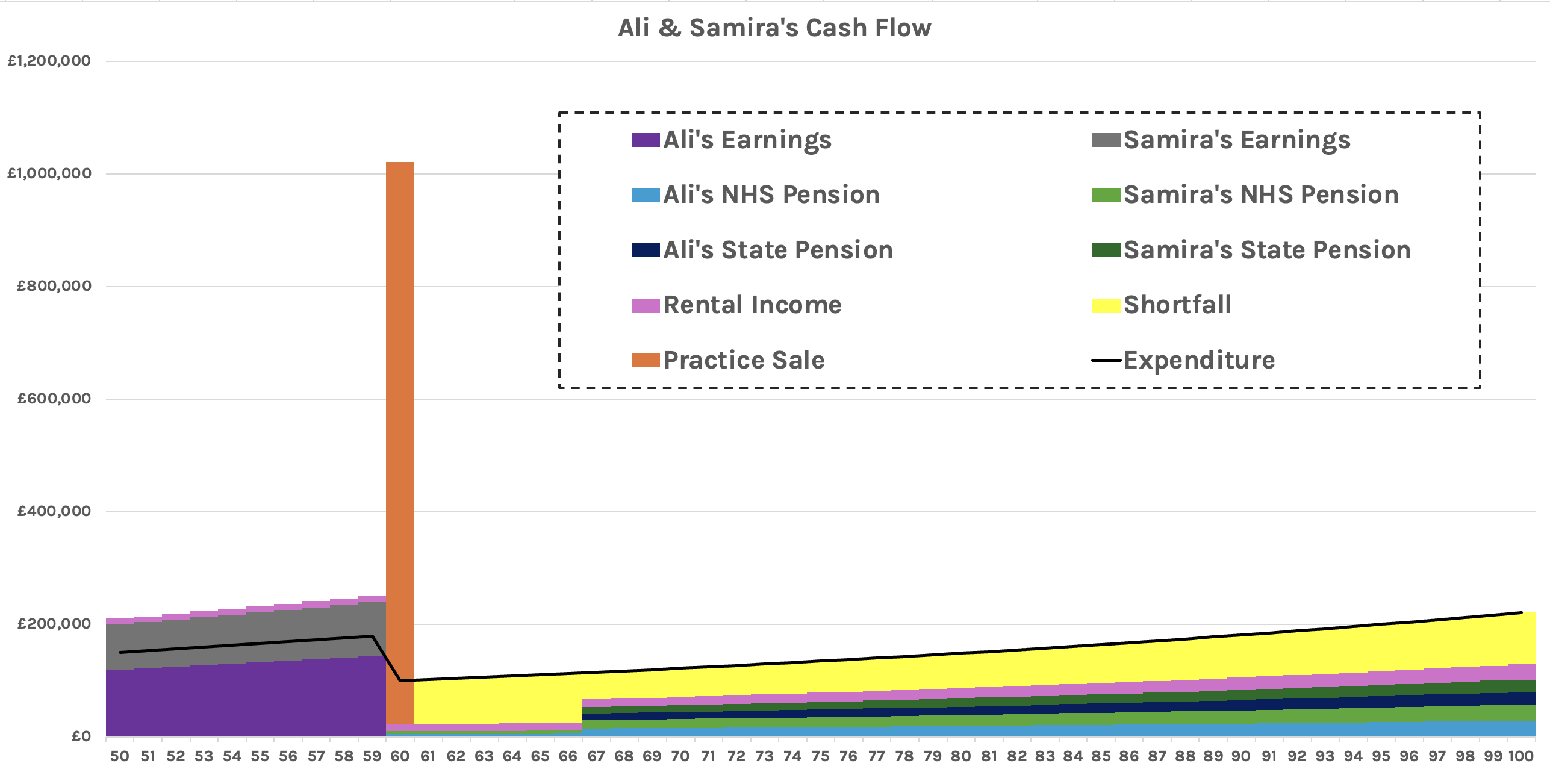

Ali and Samira, on the other hand, are in their 40s and both of them have pensions at the 2015 scheme rates. This chart is a little more complex. The couple would like to retire at 60, but our projections show that without action, this is currently unachievable.

Note in particular the orange spike representing the practice sale, and the particularly fallow period before their NHS and state pensions kick in at age 67. Even when those pensions do kick in, expenditure (black line) is too great, and there is a shortfall (yellow).

What Now?

As the old Chinese proverb says: “The best time to plant a tree was 20 years ago…the second best time is now”. The same is very much true when it comes to preparing for retirement.

Montgomery Charles are an independent financial planning company with nearly three decades of specialist experience advising dentist practice principals.

We are on hand to provide a complimentary, no-obligation consultation to help you on your journey.