The ultimate guide to planning your retirement

As financial planners, we are often asked the question “when can I retire”? The answer is always the same: you can retire at any age…as long as you have both the means and the desire.

But what does that mean in practice? This resource takes an in-depth look at some of the things you need to think about when considering your future plans.

What’s covered in this resource

Jump to:

3. How much do I need for a good retirement?

4. What guaranteed retirement income can I get?

5. Growing your income even further: using investments to achieve the retirement you want

6. Financial planning: could it extend your life expectancy?

7. Your next steps: is going alone the right option for you?

1. The desire to retire

When someone tells us they want to retire (at any age), our first question is always: why? The ‘why’ is always the starting point for lifetime financial planning, and as you can imagine the answer is different for everyone. The reasons we hear often include:

- “I have worked for many years and have done my time”

- “Running a business is stressful and I want to sell it”

- “I want to explore the world”

- “Spending more time with friends and family is really important to me”

- “My parents died young and I want to enjoy life whilst I still have time”

Having established this, our next step would be to explore in great detail exactly what you will do in all the free time you will suddenly have.

The reason for going into so much detail – before we even think about the numbers – is because retirement at any age (like life in general) is all about getting the right balance.

For example: people that are really fed up with work might go from a five-day working week to zero work overnight – and immediately discover that it comes as a big shock to the system. But those that have a financial planner working by their side are, more often than not, armed with the knowledge that they could completely stop working if they really wanted to.

With the financial aspect to retiring removed from the equation, they will suddenly find the weight has been lifted off their shoulders, and they are now working on their own terms. This is incredibly empowering, and we often see clients decide to transition into retirement over several years (even if they can afford to retire outright), and gradually transition towards retirement.

This is just one example: you will have your own reasons for wanting to retire. But once that ‘why’ is broken down in detail, you’ll be able to put a plan in place that realises your goals. And if you’re working with a financial planner, you’ll almost certainly be surprised at what’s possible.

2. The means to retire

In other words: can you afford to retire? Again, ‘balance’ is the key.

The average life expectancy for a 55-year-old living in the UK is 84 for a man and 87 for a woman, according to the Office for National Statistics (ONS). Great – so if you stop working at age 55, you need enough money to last you roughly 30 years, right?

Not exactly.

These figures don’t take into account differences in region, socio-economic standing, personal health and so on. Plus, an average life expectancy is exactly that: an average. Millions of people will die earlier and millions will die later; the average of all these is the number that sits in the middle. This might sound like morbid thinking, but it’s really the opposite: we must think positively when planning for retirement! If your plans assume you live to 85, but you actually live until age 100, you may have no money for the last 15 years of your life.

We call this the ‘flaw of averages’. It is one of the biggest risks when it comes to retirement planning, and it’s the biggest reason that there’s no one-size-fits-all approach to the topic. You will probably have seen articles online – often in a ‘listicle’-type format – that offer simple rules about when to retire. Because of the ‘flaw of averages’, these articles are completely and utterly useless.

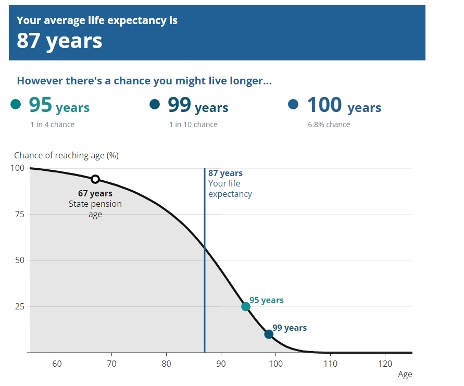

ONS predictive statistics for a woman currently aged 55

If you can see past the rather gloomy nature of the exercise, we encourage you to look at the ONS life expectancy calculator for yourself. It will also show you the chances of living to the State Pension Age, and of living to 100 years old.

In the example shown on this page (for a woman currently aged 55), there may only be a 1 in 10 chance of living until age 99. But it is a good idea to plan for living at least that long, just in case. Some people are convinced that because their parents died young, they too will die young. Sure enough, 20 years after their self-predicted death, they are still going strong – but having spent a large proportion of their retirement funds. For couples, there is 25% chance that you’ll both live to 95 and a 50% chance that at least one of you will live to 95: put that way, you can really see how you need to plan ahead for a long life.

Don’t forget the ‘doubling’ effect

Remember that for every extra year you work, you could have two years’ less to fund in retirement. That’s because in addition to your retirement period being one year shorter, you’ll have earned an extra years’ worth of savings, pension contributions, and investment growth, which will in itself fund one year of your retirement.

Other things to factor in when considering your ‘means’

There are a number of other things to consider, and all of them revolve around finding that all-important ‘balance’. These could include:

- Matters of inheritance: You don’t want to retire too late, with too much money that you will never spend or that you pass on to children when they are already older and don’t really need it. As one of our clients bluntly put it – “you don’t want to be the richest stiff in the graveyard”! But at the same time, you need to make sure you have enough to see out your days in comfort

- You’ll need to balance up whether you want to spend more to enjoy life now whilst you are still working, or to be more deliberate with your current spending to ensure your future financial security

- You might want to weigh up spending more in your earlier years of retirement (e.g. going on that round-the-world trip whilst you are still young, fit and healthy, or one-off big purchases like motorhomes and cars), against having a nest egg for later life to get the level of long-term care you may need

3. How much do I need for a good retirement?

How long is a piece of string?

This really depends on what is classed as a ‘good’ lifestyle for you. It usually follows that this is linked to the kind of lifestyle you have become accustomed to in the lead-up to retirement. It sounds like an obvious statement but the amount we ‘need’ in retirement can vary wildly from person to person.

Whatever that amount is for you, it’s important to remember that you must end up with this amount after paying any tax – which can have a big impact on which pots we need to take money from, and in what order.

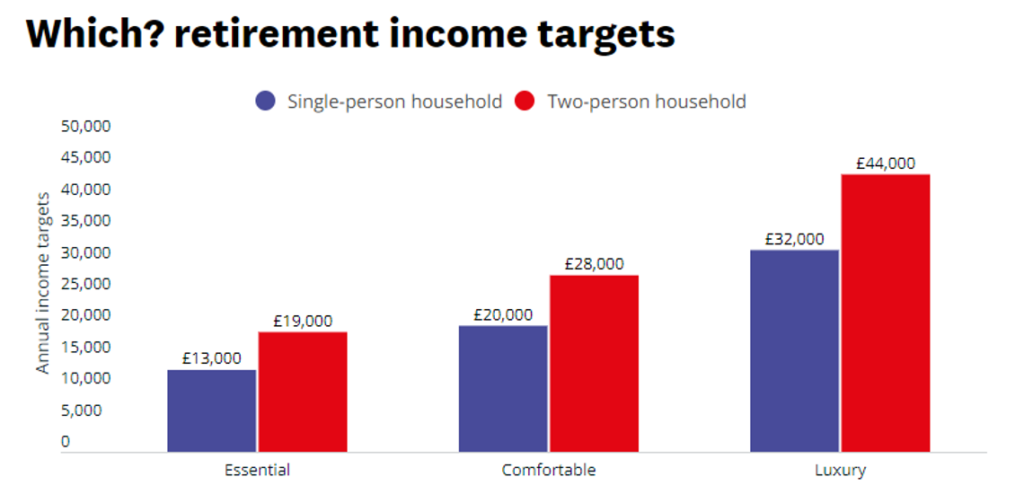

As a starting point, Which? Regularly surveys its retired members to find out how much they need in retirement for different lifestyle types.

Image: ‘Which’ Magazine

‘Essential’ spending covers everything needed just to get by (such as food, transport, utility bills, clothes, etc). The ‘Comfortable’ income target includes leisure activities, short haul holidays and gifts. The ‘Luxury’ target also includes home improvements, health club memberships, long haul holidays and a new car every five years.

Retirement Living Standards research carried out by the Pensions and Lifetime Savings Association gives a broadly similar picture, albeit with slightly higher amounts than the Which? Research. (Please do note that the figures given in both of these examples will have increased significantly over the last couple of years due to inflation.)

Image: Pensions and Lifetime Savings Association

Typically, our own clients have household retirement target incomes of £75,000+ per year and often have the ability to take income far above their targets. But ultimately, your ‘Number’ will depend on what you want to do in retirement and the type of lifestyle you wish to have.

How do I calculate my ‘Number’?

When working out what this is, you need to be very diligent in calculating not only your essential spend, but what you will actually want to spend on the ‘nice-to-haves’: the fun things in life, like going out, entertainment and holidays. Our experience tells us that around 90% of people underestimate this, so be careful – it can lead to you not enjoying the retirement you had hoped for.

We always tell our clients to dream big – you only get to enjoy one retirement! The key is to be honest with yourself (and us!) so we can properly plan for the amount you’ll need.

You will also need to think how your spending will change once you stop work. You will not have commuting costs to contend with, but you may travel more to see friends and family. You will have likely paid off your mortgage by the time you stop work, but are you spending more on activities and entertainment because you have more free time?

It’s highly likely the kids will have flown the nest by that point too – however, you may be spending money on helping them out (with house deposits, perhaps, or school fees for the grandchildren). You will probably be paying less tax than when you were working too: at the very least, you will not pay national insurance unless you continue earning money through work.

A useful rule of thumb is to assume you will need two thirds of your gross salary to maintain a similar level of lifestyle in retirement. Of course, rules of thumb should only be seen as a starting point to determine the right level of retirement spending for you personally. There is no substitute for detailed financial planning.

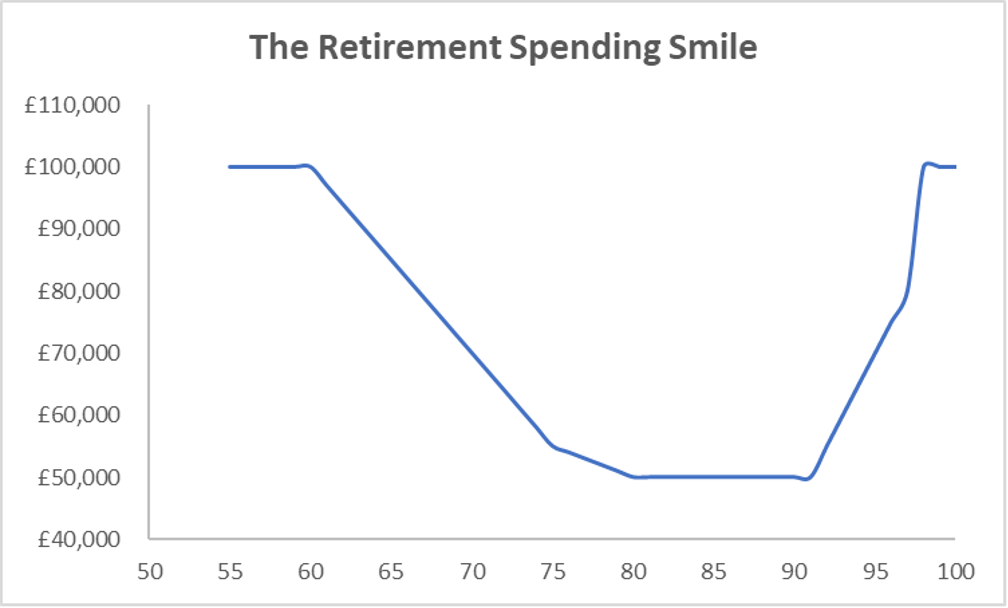

The Retirement Spending Smile

The Retirement Spending Smile principle says that people typically spend more in their early years of financial independence, because they are young and active and want to travel. Spending then typically tails off when they reach their late 70s/early 80s as they take less holidays, stay closer to home and are generally less active.

The Retirement Spending Smile principle says that people typically spend more in their early years of financial independence, because they are young and active and want to travel. Spending then typically tails off when they reach their late 70s/early 80s as they take less holidays, stay closer to home and are generally less active.

Spending may then increase again in their later years if they have to pay for care, which can last a few years.

If there are big one-off spending plans in the first few years of retirement (a new car, a motorhome, a cruise to Antarctica…) we would also take these into account when creating a client’s financial plan.

Inflation-proof planning

The amount we need in retirement will also go up with inflation. An estimation of £50,000 per year for retirement in in today’s money might, in 20 years’ time, actually translate into £100,000 per year. This is why we always need to inflation-proof our income and pots of money as much as possible. You can find out more about how this can be managed in the ‘retirement income’ section below.

I know how much I need – what’s next?

Once you know how much money you think you will need per year, the next steps are to understand how you will meet your needs.

4. What guaranteed retirement income can I get?

You should aim to get at least the State Pension, but other forms of guaranteed income are also available.

The State Pension

The State Pension is currently paid out to people who reach age 66 and have built up enough qualifying years. As previously mentioned, this age is increasing to 67 and then eventually to 68. Independent researchers have suggested this needs to increase to 71 in order for the State Pension to remain affordable for the government. Because of this uncertainty, it is vital that you also make the most of private pension arrangements (see section 5, below) to help mitigate any gaps you may face.

Once you reach State Pension Age, you can choose to delay taking your pension (which will result in a slight annual increase). However, the lost income whilst you are not receiving it can mean this is not a good idea.

You will need at least 10 qualifying years to get any State Pension and typically 35 years to get the full State Pension (broadly speaking, you are accruing ‘qualifying years’ if you are employed or self-employed, but do check the government’s own guidance for an extensive definition). Some people need more than 35 years (for example if you have been a member of a public sector pension scheme such, as the NHS pension).

The full State Pension will pay £11,501 per year from April 2024, meaning a couple could receive £23,002 per year. The State Pension does not transfer to a spouse on death.

This income is really the bedrock of your retirement planning. It is guaranteed to be paid out for the rest of your life and will increase in line with inflation (currently measured by the triple lock). This is why it is vital to ensure you will be entitled to the full State Pension before you reach State Pension Age.

You can check your State Pension forecast and contribution record via the Government Gateway. It is important to focus on the text under the forecast number in the big box. This will tell you how many more years you will need to contribute to get the full amount. If you have gaps in your record, there is a limited window to make good any shortfall and you should seek advice as soon as possible. If you do have to make up any shortfall, the State Pension is an extremely good value investment to make in your future financial security!

Other guaranteed pension income (final salary pensions)

If you have been a member of a defined benefit pension scheme (also known as final salary or CARE schemes) – for example because you work in the public sector, or have an old private sector pension, then this will provide you with an income for life. This pension income will come in on top of your State Pension and form part of that bedrock of your retirement planning. It may well get you most – if not all the way – to your income target.

There are many different schemes out there, but they all have features in common and some may provide extra benefits as well. A defined benefit pension:

- Will provide you a guaranteed pension income for life

- From a specified age (usually between 60 and State Pension Age)

- There is usually some inflation-linking as well

- If you die, your spouse or partner is usually entitled to a percentage of your pension for the rest of their life (typically between 33%-50%)

- You may be entitled to an automatic tax-free lump sum when you take your pension, or have the option to give up some of your annual income in exchange for a tax-free lump sum (known as commutation)

- You can usually take your pension before the specified age (although you can’t be younger than 55 when you do this) – however, you will likely have to give up some of your annual income to do so (usually 4% for every year early you take it)

You may also be entitled to an annuity, which again is usually an income for life and will have some or all of the features listed above.

This pension income is very valuable – because of the guarantee for life, it will not dry up as you get older. However defined benefit schemes are very complicated and it can be a minefield when negotiating all the options available to you. You only have one chance to take the right option for you, and so you should seek advice to ensure you fully understand all of the consequences. This gives you the best chance of ensuring your future financial security.

Other Income

You will need to consider any other sources of income you might have in retirement. These could include:

- Consultancy work, where people transition into retirement and can often earn very good money due to their experience, for a relatively small time commitment

- Rental income (this is becoming less favourable due to the high interest rates, tax regime and illiquid nature of property)

- Dividends from shares (for example: if you set up a business during your career, then you might retain shares in retirement)

- Deferred consideration from a business sale (where someone receives the proceeds over a number of years)

Any extra income you expect to receive will again go some way to meeting your retirement income targets. The real question you have to ask yourself here is: how long will this other income last?

And how long do you want it to last? For example: do you really want to be running a rental property portfolio rather than enjoying retirement? Or would you rather have access to the capital from the properties now?

And if your various incomes lead to a surplus? Well you can either spend it, or save it for future years when you may need it.

5. Growing your income even further: using investments to achieve the retirement you want

If your incomes do not meet your target, then this is when you will have to draw on other funds. In this scenario, you will need to look beyond your guaranteed pension income – to additional pensions, cash, ISAs, and other investments*.

Pension Pots

You may have accrued a number of different pension pots through your workplace pension arrangements and/or have built up your own private pension arrangements. The benefits of contributing to these over your career and leaving them to grow until later life include:

You receive tax relief on money you pay into a pension. For example, let’s say your annual salary is £110,000:

- The tax implications of earning over £100,000 mean that on that last £10,000, you’ll only receive £3,800 of take-home pay after tax and National Insurance

- Paying this £10,000 into a pension – via salary sacrifice – will leave you £6,200 better off!

- The trade-off? You are choosing between £3,800 in your pocket today versus £10,000+ tax-free growth tomorrow

You may see quite significant growth in your pension values – hopefully beating inflation over the time you have been invested.

Your invested pension will grow tax-free and earn tax-free dividends and interest – really benefitting from the power of compound growth (earning profits on your profit).

When you come to take money from your pension, 25% of the sum withdrawn will be tax-free – and the rest taxable at your marginal rate of tax, which could be lower than when you were working. This can ensure you take out what you need, when you need it – paying as little tax as possible and leaving the rest to grow over the remainder of your lifetime.

And finally, money you do not spend that is left in your pension pots when you pass away can be inherited by your loved ones, free of any inheritance tax.

Pensions are a highly complex area and it is vital to seek advice to help you make the most of them as part of your overall financial plan.

With the right advice you can ensure that you are: making the most of the tax relief on your contributions; investing your funds in the right way; gaining access to powerful features and benefits in terms of accessing your funds and passing them on to your loved ones; and knowing how much to take from your pension, when and in the best way, to meet your retirement needs.

ISAs & other investment vehicles

If you have the opportunity to make the most of the ‘use it or lose it’ annual ISA allowances (£20,000 per person) then you can build up an additional pot of money that you can put towards your retirement.

Like pensions, funds you hold in ISAs benefit from tax-free growth, dividends and interest. You do not get tax relief on your contributions, but you do not have to pay tax when you withdraw your money.

In addition, there are a number of other types of investment wrappers, within which you can build up a pot of money to help you fund your retirement needs – the stock market, for example. We’re not going to get into this area here as it merits a whole guide in itself – but as with many aspects of retirement planning, it’s vital to seek expert guidance before plunging into this area.

Putting it all together

If you use your money wisely and invest it, then you could benefit from investment growth to make up any shortfall between your retirement incomes and your planned expenditure. Remember that investment growth does not stop at retirement, and that you need only draw what you need each year, leaving the rest invested to continue growing over the rest of your life.

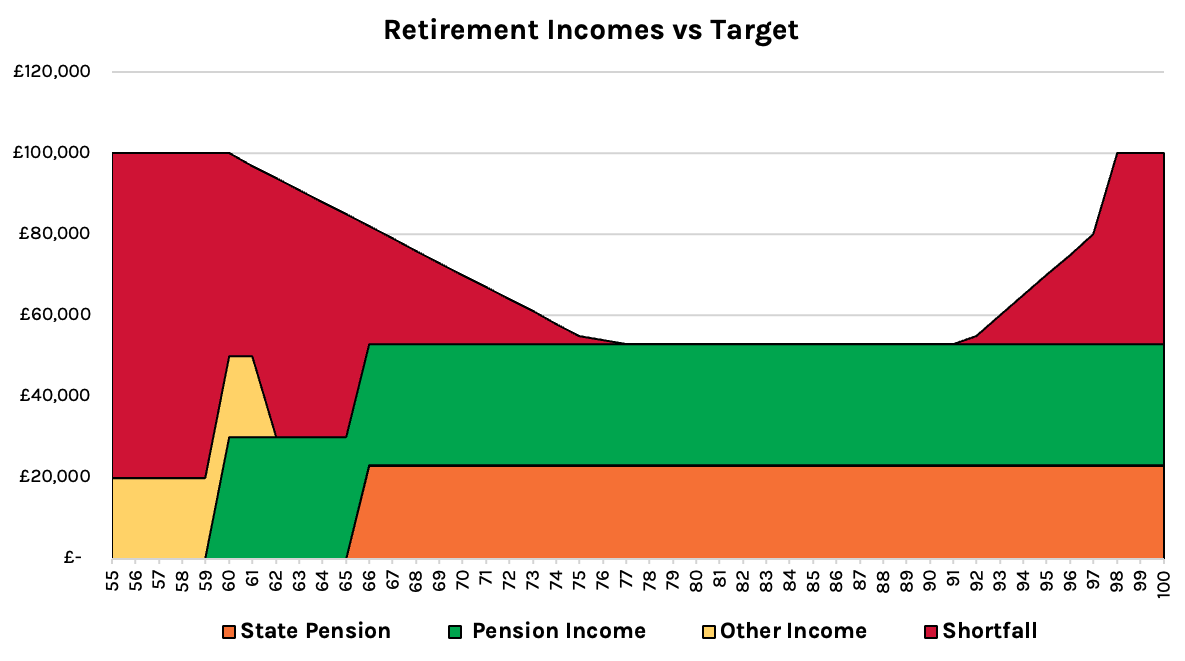

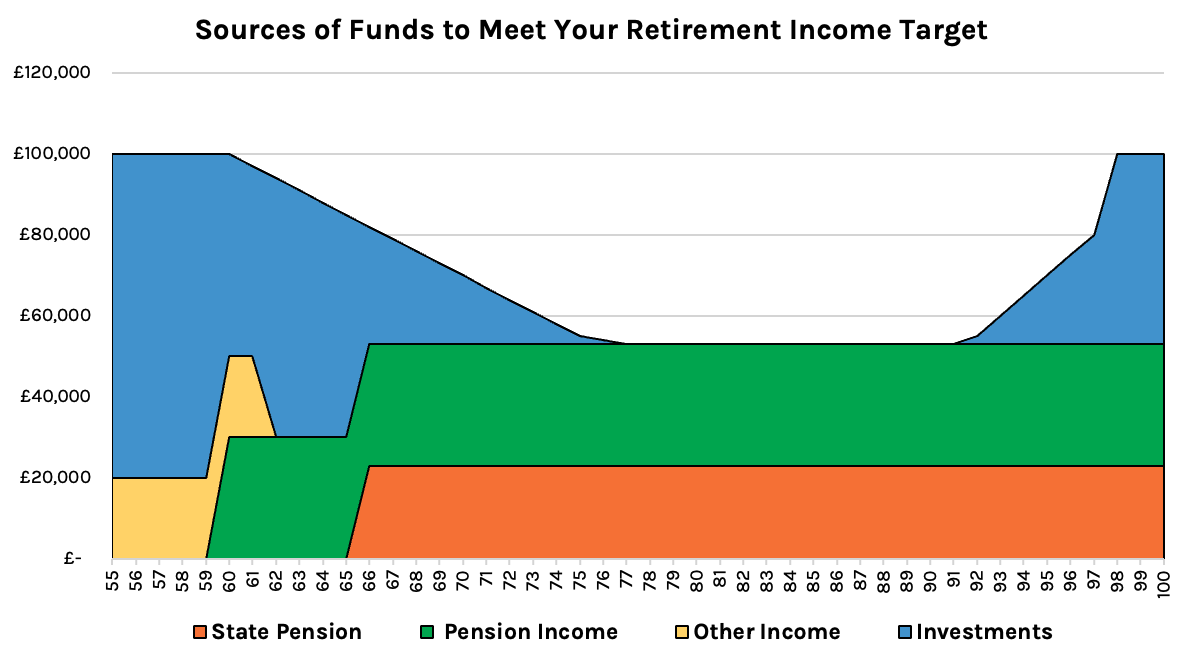

To illustrate this, here’s an example of how additional investment could meet the needs of someone hoping to retire at age 55.

The black line at the top – ie, the line dividing the white space from the coloured space – represents the target retirement income. You may recognise the ‘Retirement Smile’ shape from earlier in this guide:

You can see the dark blue section is the State Pension, kicking in at age 66. In this example there is also a final salary pension (green) that starts at age 60. By the time both of these are in payment, a large chunk of our retirement income is being met (helped by the fact that there is less spending going on in this period of life).

We have also got some additional income (yellow) in the early years of retirement, due to consultancy work. But as it stands, this income is not enough to make up the shortfall (red).

However if we use our retirement pots to fill our spending gap, then we should have enough to get rid of the red. Let’s say we have an investment pot of £1 million, and we achieved 4% growth a year on those investments. The spending picture would now look like this:

We can see that we are drawing on just enough of our investments (blue) to meet the gap.

Investing your money also gives it the best chance to at least maintain its value against inflation over the long-term and to grow enough to meet any shortfall in later life. Cash doesn’t usually keep up with inflation – just look at how the cost of goods are rising today, in comparison to the interest rates on your savings. If you leave all your money in cash, then it will lose value over time, and you are more likely to run out of money in your retirement.

Some of your money will therefore be invested for many, many years, while some will be invested for only a very short period of time. It is important to get the balance of your investment pots right: you do not want your short-term pot to be too small, with not enough accessible cash; nor do you want your longer-term pot taking too little risk, because it may not grow enough to meet your needs in your later life.

When taking money out of investments to meet an income shortfall, we also need to be aware that we may have to pay tax. For example: you may have to pay tax on money you take from pension pots, but you do not owe any tax when taking money out of ISAs. All this needs to be factored in to your long-term plan.

Financial planning: could it extend your life expectancy?

Be warned that working with Montgomery Charles is likely to make you live longer! A recent study has found a correlation between good financial planning and increased life expectancy. Okay, this correlation hasn’t been proven (yet!) – but it’s not hard to imagine how this could be true.

- The stresses and strains of managing your own finances and planning for the future should not be underestimated. The reassurance of having an expert by your side, doing this for you, can relieve this burden

- Those who work with a financial adviser a number of years before they want to retire, rather than at the point of retirement, will likely be in a much better financial position due to taxes saved, investment growth and other factors. This means that our clients often retire several years before they originally planned to when they first started working with us – an obvious reduction in stress at a key stage in their lives

- More time spent doing the things we want to do (both pre and post-retirement), is likely going to mean we are happier, healthier and live longer

- Our clients have more money in retirement and so are able to live the lifestyle they want to live. Because we always encourage our clients to ‘get more life out of life’ (our motto), we are helping them ensure their money is always working in the best way for them

This is why we always plan for a client to live to at least 100 and sometimes beyond!

Your next steps: is going alone the right option for you?

There is an old Chinese proverb that says “The best time to plant a tree was 20 years ago. The second best time is today.” This completely sums up planning your financial future. It takes time to develop a plan and grow towards achieving your goals, and the sooner you start, the better. But even if you have left it late, it’s still far better to act today than to do nothing.

While it’s possible for anyone to get a rough idea of what their retirement might look like, the complex issues involved really do mean it’s best to speak to a financial planner.

Here are some of the ways in which we would help you with the process:

- Working together to uncover and formalise your goals (our ethos is to help people ‘get more life out of life’ (our motto) and so goal-setting is always the first step

- Building a Financial Life Plan to determine when you can retire and what your retirement will look like, taking into account your current and future incomes and investment pots

- Determining a spending plan so you can still live life now, balanced against the future that you want

- Developing a tax-efficient contribution plan to build a multi-pot portfolio and ensure you are investing enough money in the right type of pots, saving the most tax possible (more tax saved = a better retirement)

- Implementing an evidence-based, globally-diversified investment strategy, aligned to your comfort levels with investing, to ensure your hard-earned money is working hard for you and your future

- Helping you maximise the sale value of your business and any subsequent work and income terms

- Determining when and how best to access your various retirement and pension incomes and whether to turn your investment pots into annuities

- Building a dynamic and tax-efficient withdrawal strategy to ensure your investment pots last as long as possible and continue to grow in the meantime

- Determining whether there is a need to release equity from your property in later life

- Building a succession plan for the next generations and ensuring your wealth stays in the family

- Staying by your side and continuously updating your plan, so you can still meet your goals, no matter what life throws at you. We know the journey is never as easy as from A to B, it is often via C, D and E.

- And of course, potentially increasing your life expectancy!

If you’d like to speak to a financial planner and start your retirement planning today, schedule a no cost, no commitment consultation with one of our experts.

*Remember that investment growth is not guaranteed and you will need to seek specialist advice based on your own financial position.