By James Whittington, Chartered Financial Planner at Montgomery Charles

As a nation, one of the socioeconomic problems we face is that of an ageing population – and the same is true of the financial advice industry.

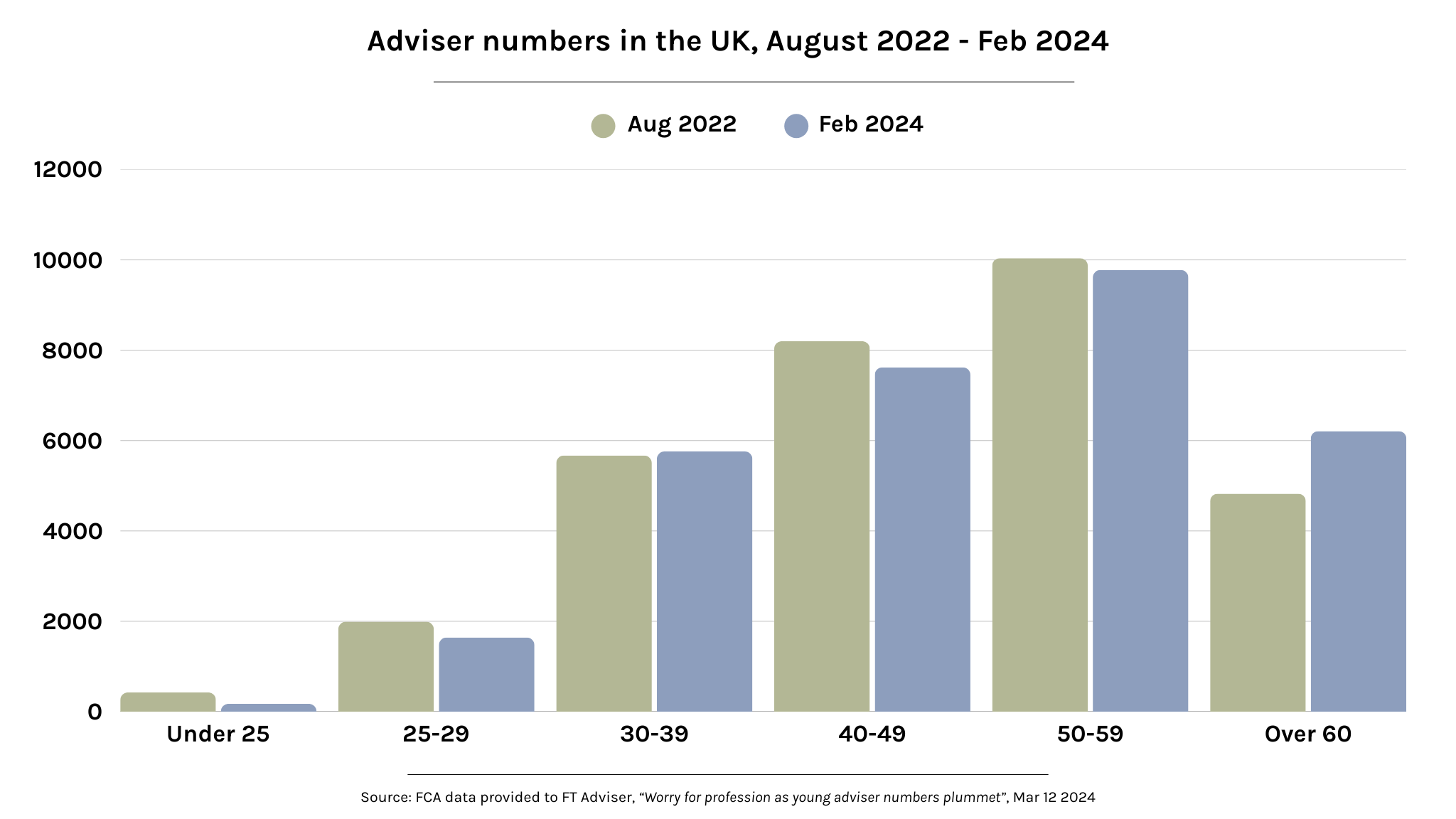

Based on an FT Freedom of Information request to the FCA in February 2024, 20% of all financial advisers in the UK are aged over 60 and 51% of all advisers are aged 50 and above. Conversely, only 6% of advisers are aged under 30, and only 24% are under 40. This is the reverse of an age profile you would expect to see in most other professional sectors. (For example, more than half of doctors are under the age of 40.)

When digging into the numbers and comparing to 18 months prior, it is clear that the number of older advisers is growing, but the age brackets below are not being replenished. Younger advisers are leaving the sector and fewer younger people are choosing to join, instead preferring other areas of the financial industry such as banking and accountancy.

Is my financial adviser likely to retire soon?

A survey of financial advice clients, carried out by Investec, showed that 41% of people think their adviser will retire in the next 5 years (and 21% in the next 2 years). 46% of clients were “quite” or “very concerned” about their adviser retiring and what it would mean for them.

Other surveys show that clients are right to worry, with 50% of advisers actually planning to retire in the next 5 years. The average planned retirement age of financial advisers looking to retire is just 52 years old.

Why are so many advisers retiring?

Why are so many advisers retiring?

One reason may be the increased regulatory burden over the last couple of years. A CoreData survey of advisers in 2023 showed that 1 in 10 were thinking of leaving the industry because of the introduction of Consumer Duty. No matter how admirable the intentions of the new regulation, it undoubtedly presents a cost in terms of both time and money to some companies and has been accused of taking a heavy toll on the mental wellbeing of a large number of advisers.

We know, too that people skew towards taking financial advice from professionals from a similar demographic background to themselves, regardless of the adviser’s qualifications and experience. No young person wants to wait around to get older before they can earn a decent living – which means there is no obvious ‘conveyor belt’ of young advising talent.

What happens if my financial adviser does retire?

This really depends on how your financial adviser operates.

For example, if they own the practice, they will most likely look to sell the company on to either another individual, who may or may not work there already – or to a larger company looking to acquire smaller practices.

In just the 18 months to February 2024, there was a 7% drop in the number of financial advice firms. It is highly likely a number of these were acquired by bigger ‘consolidators’.

The same is true when advisers operating under a network (such as St James’s Place or Quilters) want to retire: the network does not want to lose the clients and the future income those clients will generate. In this case, the company will look to either buy the client book off the retiring adviser, or help another adviser within the network to purchase that book of clients (in some cases, by directly financing them).

In this scenario, what is somebody buying when they purchase a financial advice firm? Well to put it bluntly: they are buying YOU! The book of clients a firm has is their main asset to generating future income and ultimately profit. You are, in effect, your adviser’s pension – when they sell you on to another firm, they are receiving their retirement pot that enables them to hang their boots up and sail off into the sunset.

So what’s the problem?

Are you really just a transaction?

Put simply, this ‘transaction’ is unlikely to be happening with your best interests at heart.

This is because the retiring adviser usually gets paid off across several years – meaning they are financially incentivised for you to stay with the new adviser for a decent period of time. And the new adviser doesn’t want you leaving after having just forked out a large lump sum to buy you.

Furthermore, you have not ‘picked’ your new adviser, and they have not ‘picked’ you. Are they the most suitable person for you to place your trust (and life savings) with? Who knows.

Not only that, but because of the aforementioned issues with increased regulatory burdens and costs, and more firms being purchased by consolidators, there is a high chance you will have just gone from receiving independent financial advice to receiving advice that is not independent and may not be suitable for your needs.

And if they are of an average age for a financial adviser, who is to say you will not be going through this process again in another five years’ time?

Getting ‘offboarded’

It’s not nice to hear, but clients may even find themselves without an adviser if the new firm doesn’t deem them worthy enough to carry on servicing them.

Data shows that the number of clients that financial advisers have ceased servicing has been going up, year-on-year for the last 5 years, with 204,620 clients being ‘offboarded’ in 2023.

The Montgomery Charles way

Our team

I’ve talked so far about the difficulties that can come with your adviser retiring. But for smaller firms like Montgomery Charles, it can, thankfully, be very different.

We do not view our clients as assets. We see ourselves as financial partners to help our clients achieve their life’s goals and ambitions. We will always be independent. We don’t ‘own’ you, which is why there are never any tie-ins or exit fees for our clients.

We have strong business continuity planning in place – if and when an adviser decides to retire, there is an in-depth plan to ensure a seamless transition for our clients to the right adviser for them. There is no ‘buying and selling’ of clients, as this is fundamentally against our ethos.

Finally, we are working hard to train the advisers of the future, with a strong adviser training programme in place – a fascinating career path for anyone in our organisation that is interested in taking that step.

So what should I do if my adviser retires?

A seismic event like this is the ideal time to weigh up your options. You may have been with your adviser for several decades and a lot has changed over that time – in terms of the industry, the regulatory landscape and your own circumstances.

When taking on clients whose advisers have retired, we often find that their financial planning (and ultimately their financial adviser) had not kept pace with all these changes, and that there are a lot of improvements that could be made to their circumstances.

Here are our top tips for how to approach this process:

- Get a second opinion on your financial planning! We would actively encourage you to hold a ‘beauty parade’ and interview several financial advisers, to find the best fit for you. This would be someone that:

- Is used to dealing with people in your situation and has the relevant experience, knowledge and qualifications to do so

- Has the capacity to take you on and provide you with the level of service you need (that includes having a good team that enables the adviser to provide you with the service you need)

- Is independent

- Works for a company that is structured in the right way to ensure you are always treated in the right way

- Remember you are under no obligation to move to the new adviser or firm that is being presented to you

- Challenge and question whether you are in effect part of the deal between the retiring and the new adviser

It’s not fun

We know that many of you have built up a trusted relationship – and often even a friendship – with someone that has been by your side for decades. Advisers are often privy to a client’s innermost thoughts and feelings, have an intimate knowledge of their family situation and usually the first port of call when life throws things at them.

The prospect of that person hanging their boots up, forcing you to forge that type of relationship again with an unknown person, is daunting.

If you think your adviser may be retiring in the not too distant future and you would like an independent, second opinion on what this means for you, feel free to book a no cost, no commitment, informal chat with one of our advisers today.

Any money invested carries an element of risk and you are not guaranteed to get back the money you invested. This article does not constitute advice and you should consult your financial adviser prior to any action.